Terry Lynch

is a licenced mortgage agent with TMG, The Mortgage Group. In addition to conventional mortgage funding, lines of credit, commercial and construction loans, Terry also specializes in Challenged Credit and Reverse Mortgages. He also secures funding for a variety of businesses such as retail, restaurants, franchises etc.

Terry is also a Director on the Executive Board of the Uxbridge Chamber of Commerce.

416-315-1787

[email protected]

The Damocles – “Two-edged Sword” of Real Estate

Following is an overview illustrating the role leverage is playing in a wild and often topsy-turvy Real Estate market like we are experiencing in Uxbridge right now.

Leverage

Nowadays, as compared to some 40 years ago, with $100,000 of income, a creditworthy borrower can now qualify for almost three times the mortgage that would have been possible in the early 1980s.

As a result of decades of falling interest rates combined with expanding credit availability, borrowers have been able to access a proportionately bigger ‘piece of the rock’, all of this acting as a catalytic lever for home values and mortgage activity. Even though the prosperity that’s been created in this millennium is truly unprecedented, it’s largely thanks to a rocket-like vertical climb in real estate.

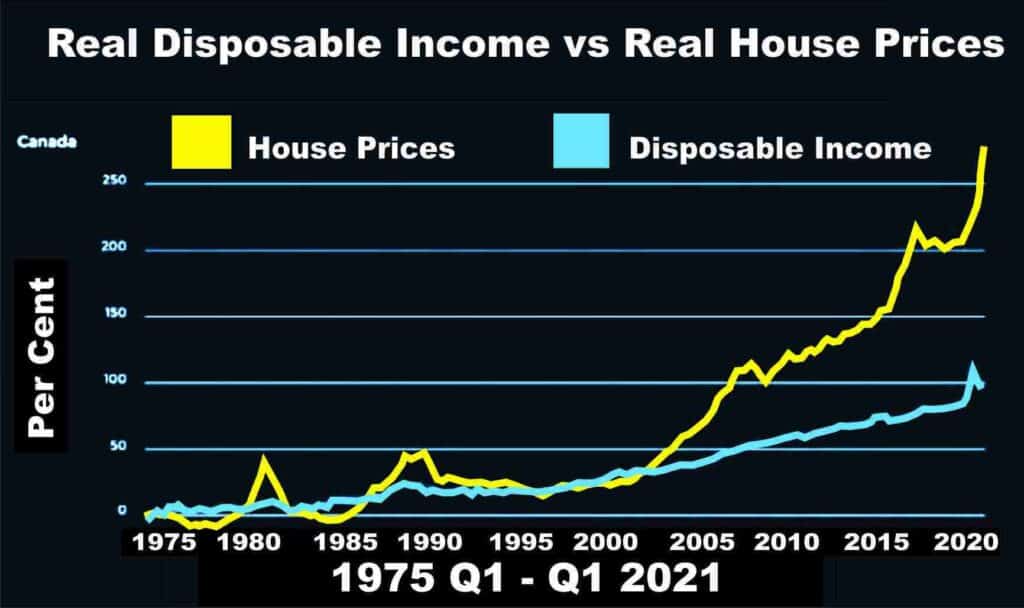

The accompanying chart illustrates perfectly the results of real estate leverage, or, in other words, the meteoric rise in housing prices as compared to the much lower rate of income growth:

Home prices rise faster than disposable-income growth

Some fifteen years or so ago, naysayers in the housing business started to opine that home prices were deviating from fundamentals. The attached graph shows what happened next!

The market had its own ideas about which “fundamentals” were important.

And of course, housing the same naysayers said the very same thing ten years ago. Five years later, echoing the same warning. Today, they’re saying it again. But this time, they may be getting closer to being right.

Catalysts change

Contrary to naysayer disinformation, real estate values don’t rise on air. Prices—and those of us who practice our businesses as mortgage brokers—would never be at today’s heights if not for fundamental forces (e.g. falling rates, rising incomes, population growth, urbanization, supply shortages, etc.). people are prepared to pay ever more for properties because actual fundamentals give them reason too.

But fundamentals are mercurial. They can change.

When prices get so unrealistic in terms of affordability that Canadians making above-average incomes can’t afford even average homes, supply adjusts. It must.

Of course, so far it hasn’t, at least not to any noticeable degree. But, with enough time and extremes prices, supply always adapts. That’s been true all throughout history, even if only for a short time—whether driven by developers in search of excess profits, by governmental policy or by shifting trends (like work-from-home or high-speed commuting, which makes building on cheaper land economically viable).

What’s at stake?

Compared to 20 years ago Canada’s economy relies twice as much on residential investment to fuel GDP. For the first time ever, residential investment like new construction, renovation services, mortgage brokering and real estate services total over 10% of GDP.

In all, residential investment accounted for a remarkable 54% of GDP gains in the first quarter, according to Edge Realty Analytics.

Residential investment as share of GDP

Canada’s economy literally cannot afford any diminution in the housing business. Leverage is a powerful entity until you run out of it.

When interest rates climb the two-way sword of leverage cuts in the wrong direction. And according to the financial pundits, if one believes implied pricing in the bond market, rates are headed roughly 175 basis points higher in the next 24 months.

Once rock-bottom rates are removed from the equation after a parabolic price increase—let alone after other credit tightening such as tougher qualifying rates or limits on amortizations, debt service ratios or non-prime lending—just watch the magic of leverage work in reverse!

No financial maven has the cojones to predict when the housing tide may turn, but it will ultimately turn, for the following reasons:

In expansionary cycles, inflation always exceeds the Bank of Canada’s 2% target long enough to warrant rate hikes.

The market will hit a point—if it hasn’t already—where average incomes are simply insufficient to qualify for financing on average homes.

Supply will catch up, be it from new listings by nervous sellers hoping to lock in windfall capital gains, government initiatives, or just good old developer greed (the productive greed that incentivizes development).

With the hopeful expectation that the COVID pandemic will at some point be over, many downtown office workers who fled to the smaller communities to get a better ‘bang for their buck’ will more than likely be asked (or commanded) to return to the physical, (rather than the virtual) workplace. This again could cause changes in the housing dynamics as the reality of an agonizing commute to downtown sinks in.

When all this happens, industry professionals and homeowners (those who dread the thought of losing their accumulated home equity) will inevitably witness a new real estate cycle…one where leverage works in reverse!

Uxbridge Housing Rankings

(a comparison of 23 Communities in the GTA)

- Turnover (Percentage of Homes sold for ‘over listing’ in the last 23 days). Ranking: #2

- Days on the market – 9 days. Ranking: #16

- Price Growth (The change in sale price from the same period last year) Ranking: #9 25.7%

- Median Price: (If the average price is skewed, the median is a more accurate reflection of the market). Average price: $1.5miillion, Median price:$1.3million Ranking #10

More to explorer

The Uxbridge Chamber of Commerce is now closed April 19th 2024

April 19th 2024 As you know, for some time now we the board at the Uxbridge Chamber of Commerce

“From Zero to LinkedIn Hero” – A Durham College Partnership “Sold Out” Event

An amazing Event! On February 9th, the Uxbridge Chamber of Commerce in partnership with Durham College and Leslie Hughes of Punch!media put

Durham College announces partnership with Uxbridge Chamber of Commerce

Happy March Chamber Members, We are so pleased to announce our partnership with Durham College for 2022. We are one of eight